Vulnerability to poverty: Public, private, and community responses

4 Vulnerability and risk management: Dealing with shocks

This section discusses how institutions, human capital, household decisions, and community cooperation can help mitigate shocks or reduce vulnerability.

Negative economic shocks impact a household’s ability to earn income, thus affecting their economic situation and well-being. To deal with these shocks, households have different decision-making mechanisms based on the endowments they possess.

Endowments allow households to reduce their risk exposure to shocks and help smooth consumption and income. Figure 13 shows six types of endowments that act as shock mitigation tools: human capital, physical assets, financial assets, private insurance, community-based safety networks, and government policies.

Figure 13 The six types of endowments used as shock mitigation mechanisms.

Private solutions

Private responses to income shocks are mechanisms that rely solely on household resources and decisions. For instance, purchasing insurance against a natural disaster that could destroy a home is a typically private form of protection against such shocks. These protective measures depend on the household’s endowments, and the decision to implement them, even with sufficient income, may also hinge on financial literacy, which in turn is influenced by the household’s level of human capital.

Asset accumulation: Human capital and physical assets

Human capital allows the development of skills and knowledge that can be used to access more productive, formal, and higher-paid jobs in the labour market. Households with higher education and specialized skills have a higher income level, greater probability of social mobility, and lower risk of vulnerability. In addition, people with a high educational level (such as a university degree) are more adaptable to different work environments. In other words, they can retrain themselves more easily to find job opportunities according to market demand.

With unexpected income shocks, a common action affecting human capital accumulation at the household level is having inactive family members enter the labour market to compensate for the decrease in family income. For vulnerable families, it is hard to keep young members in the educational system during economic crises. Families face a trade-off between continuing to bear school-related costs such as transportation, tuition, school supplies, or uniforms with the possibility of increasing their younger family members’ future earning potential, or allowing these family members to leave school and start working, potentially bringing in extra income for the household in the short term. This reduces the capacity of low-income families to increase their human capital endowment for the future.

- collateral

- An asset that a borrower pledges to a lender as a security for a loan. If the borrower is not able to make the loan payments as promised, the lender becomes the owner of the asset.

Physical assets, such as properties, cars, livestock, land, and technological devices, can be used to smooth income during fluctuations. Households can generate additional income by renting, selling, or using assets as collateral for informal or formal loans. For example, in highly vulnerable households, pawn shops are typically used. These are places where household possessions, such as appliances, pots, or jewellery, can be used as security for a loan: if a borrower fails to repay the loan, the lender can keep the collateral in place of the unpaid amount.

Financial assets

Financial assets such as savings and access to formal or informal credit are important response mechanisms for effectively mitigating unforeseen drops in income. These resources act as a safety net in times of crisis, providing emergency income at times of greatest need, allowing households to cover their basic needs and stay out of poverty.

Going back to the example of the Del Castillo family, who had access to the formal financial market, during an income shock they could take out a bank loan at a reasonable interest rate to maintain their lifestyle. The Del Castillo family’s financial endowments significantly reduce their vulnerability and exposure to risk. Their ability to smooth their income and consumption while avoiding poverty is enhanced by the availability to them of financial assets. In contrast, the Rodriguez family lacks the necessary guarantees (such as collateral) to ensure that they can pay a loan or allow them to save, which results in the absence of formal financial endowments and access to credit. Therefore, in an economic shock, their financial response mechanism would probably be to obtain informal credit from neighbours, family members, and friends, or high-interest loans from markets not regulated by governments.

Informal credit includes less-favourable options, such as loan sharks and local gangs, who use extortion and violence to maintain control over neighbourhoods. Interest rates for these private loans are usually very high, there is a fast approval process and short repayment terms; abusive practices, such as harassment or intimidation, can also be employed during the collection process. This last point is particularly critical because such abusive practices can expose families to further risks, including extortion, threats, and violence, putting them in a more vulnerable position.

Private insurance

Insurance protects households from the effects of shocks. These insurance systems can be formal or informal. Non-vulnerable households can access formal insurance, which includes purchasing health insurance, home insurance, and accident insurance. For vulnerable households, access to formal financial resources and services may be limited, so various forms of informal insurance can help protect its members against risks and emergencies.

Informal insurance mechanisms include community support networks, which are informal agreements between family members or neighbours to help each other if needed. There are also informal savings banks, which are organisations or institutions that function as banks and provide services such as savings accounts for an agreed period. In these savings banks, there are often no interest returns, and trust or community norms are used to ensure repayment.

Community-based safety networks

- social preferences

- An individual is said to have social preferences if their individual utility depends on what happens to other people, as well as on their own pay-offs.

- altruism

- Altruism is a social preference: a person who is willing to bear a cost to benefit somebody else is said to be altruistic.

- inequality aversion

- A preference for more equal outcomes and a dislike of outcomes in which some individuals (even if they include oneself) receive more than others.

- reciprocity

- A preference to be kind to or to help others who are kind and helpful, and to withhold help and kindness from people who are not helpful or kind.

Households often belong to networks that also operate as a support system, which originates and operates at the local level. These support systems usually emerge from social networks where neighbours, relatives, or friends participate. These networks and communities are based on social preferences, which include altruism, inequality aversion, and reciprocity. Individuals are willing to sacrifice personal or material well-being to sustain these community networks because these networks improve the well-being of friends, family, and neighbours.

The iddir (or eder or idir) is a social institution in Ethiopia that is utilized for mutual aid and provides cooperative insurance within specific communities. It is an organization that primarily supports individuals with self-help activities and infrastructure development and assists bereaved families with funeral expenses and other security issues within the community. It is one example of how cultural traditions and economic functions overlap.

Community-based networks offer exchanges of several kinds, some of which complement and some of which substitute the role that government-based safety nets play. These institutions have existed for millennia and emerged as social protection mechanisms even before the appearance of the state. The persistence of these institutions show their effectiveness in reducing vulnerability. One of the oldest institutions of this kind is the iddir, an Amharic term in Ethiopia that refers to a community-based insurance mechanism in which members regularly contribute a small financial amount. This way every household can have their minimum financial needs covered for the funeral of a deceased family member.

These community networks can operate in various ways to offer social protection against vulnerability risks. First, groups of friends, neighbours, and family members can provide in-kind goods and services in exchange for cash, where both the cash and in-kind goods and services can be either given now or in the future. These agreements can be motivated by the expectation of future reciprocal action from the recipient back to the donor, a desire to reduce unfair distributions within the group, or simply a preference for making an altruistic donation to someone in the group.

ROSCAs have various names in different countries, such as tandas, pollas, cadenas, natilleras, or cundinas in Spanish-speaking countries; shamas in Swahili, kameti in Pakistan, visi in India, or hui in China.

A second type of community-based institution is an organized arrangement to protect community members in case of idiosyncratic or group-level shocks, or in other words, protection for providing services to all. These arrangements, such as the iddir, have formal and informal rules and a basic structure of governance, which include clear guidelines about rights and duties for group members so that individual contributions generate a set of goods and services, including cash, that protect the group against these shocks, or provide aid for those in need. Another example of a community-based institution is the ROSCAs (rotating savings and credit associations), which operate through a self-governed arrangement where members contribute an amount of cash periodically, and, over that timeframe, every member ends up obtaining the total amount contributed by the group in one period.1 ROSCAs offer various advantages over the formal banking system. While the interest rates are usually zero, ROSCAs have fewer formal requirements on collateral than commercial or state banks, and instead use peer pressure and trust from members of the ROSCA as a commitment device. Also, under the random allocation of the lump sum, the average member will receive the goal amount sooner than if they instead saved the periodic amounts over the total period of time to obtain the same amount.

To understand how this arrangement works, suppose the Rodriguez family wants to save $1,000 to buy an appliance. If this household can save only $50 per week, it would take 20 weeks to save the $1,000 needed. However, if 20 people join a ROSCA, and each household saves the same $50 weekly for 20 weeks, there will always be $1,000 available for any member in any given week. The most straightforward way of allocating the $1,000 every week is a lottery. The average participating household will get the $1,000 sooner than saving on its own, and in the worst-case scenario of the lottery (being the last household picked), they will still face the same outcome as saving individually over the 20 weeks.

To learn more about the broodfonds, see Vriens, Eva, and Tine De Moor. 2020. ‘Mutuals on the Move: Exclusion Processes in the Welfare State and the Rediscovery of Mutualism’. Social Inclusion 8(1): pp. 225–237.

The ROSCA institution also serves as a self-commitment device if the close ties of the 20 households include social norms such as ostracism for not complying, a sense of belonging to the group, and the well-being coming from feeling that fellow group members are also benefiting from the weekly savings each household is making. Such a self-commitment device can solve the problem of high impatience and the temptation to use the cash saved individually. These ROSCAs are common in many countries where access to formal credit is difficult or costly. The ROSCA groups rely highly on the trustworthiness of the person in the group in charge of administering the fund. Often, the ROSCA organizer is the first one to receive the money as an exchange to cover the transaction costs of contacting every member in every period and managing the cash involved. This arrangement does not exclude the group from risks. Fraud and defaults from members or the main ROSCA organizer will immediately affect the rest of the group members. Trust becomes one of the main assets to reduce such risk and therefore, via trial and error, members self-select into trustworthy ROSCAs over time.

These arrangements have evolved into credit and savings cooperatives, often under the supervision of government financial regulators. Even in countries with well-organized financial sectors, these community-based mechanisms have sometimes emerged as a response to labour market difficulties. One example is the broodfonds in the Netherlands. Here, self-employed and independent entrepreneurs are not protected by unemployment benefits from the government as they do not have a labour contract with an employer.2 In a broodfonds, each member contributes a monthly amount; if they fall sick and are unable to operate their business, they can receive a basic income. Today, more than 30,000 entrepreneurs are associated with more than 600 broodfonds groups in 200 different localities in the country. Interestingly, the group size starts at 25 people and should not be larger than 50, most likely due to the importance of maintaining the proximity and the social norms associated with the sense of belonging, social control, and commitment to a small community. If more people express interest in joining a broodfonds that is already ‘full’, a new fund is created from scratch.

Question 5 Choose the correct answer(s)

How do community-based safety networks operate to protect members from economic shocks? Read the following statements and choose the correct option(s).

- Community-based networks are often formed of individuals who cannot access formal financial services, or find it difficult and costly to do so.

- Community-based safety networks rely on reciprocal exchanges and collective support, which help members during economic difficulties.

- Community-based networks are informal and do not rely on government support.

- Community-based networks use reciprocal exchanges of goods, services, and cash between members. Savings accounts are not a key feature of community-based networks.

Exercise 5 The broodfonds

Aside from social norms, suggest some other reasons why the 25 to 50 members range is the preferred group size for a broodfonds.

Social security and government support

State support plays a vital role in improving people’s quality of life, and the support of community networks can complement it. The state can provide financial assistance, essential services, and access to healthcare and education. These all increase the endowments or income streams that poor and vulnerable households have and thus reduce their vulnerability to poverty. Remember the example of the Gonzales and Rodriguez families, where (all other things being equal) the Gonzales family is less vulnerable because they live in a country with a state protection network. Families can use the insurance that the state grants as a risk mitigation mechanism.

Countries with a well-structured network of aid and social coverage guarantee that low-income inhabitants become more resilient to economic shocks and that there is more social mobility. These circumstances facilitate the transition of households from being vulnerable to being middle class.

There is some debate about the labour market impacts of minimum wages, but there is evidence that in high-income countries, minimum wage laws have minimal effects on employment while significantly increasing the incomes of low-wage workers.

Many crucial social insurance policies can help prevent households from falling into poverty after income shocks. By providing financial assistance and support, these programmes can help protect families from economic hardship. Some of the most effective include:

- Lump sum transfers: One straightforward policy to prevent households from falling into poverty is providing lump-sum transfers (a single, unconditional payment). Usually, this policy is combined with linear taxes (a constant tax rate at all income levels). Conditional cash transfers are another successful policy (some examples are given in the ‘Find out more’ box in the next section), and evidence suggests that regular smaller payments can have better impacts than one larger lump sum transfer.

- Unemployment insurance: This programme provides temporary financial assistance to workers who have lost their jobs through no fault of their own (for example, layoffs or company closures). It can help to bridge the income gap between losing a job and finding a new one and prevent households from falling into poverty during this time.

- Disability insurance: This programme provides financial assistance to workers who become disabled and unable to work. It can help protect households from losing income and becoming impoverished if an earner becomes disabled.

- Health insurance: This programme provides financial assistance to cover the cost of medical care. It can help prevent households from going into debt or becoming impoverished if they have a significant medical expense.

- Pensions: This programme provides financial assistance to retirees. It can help to prevent households from falling into poverty once they reach old age or retire.

- Childcare subsidies: This programme provides financial assistance to help families pay for childcare. It can help keep parents in the workforce and prevent households from falling into poverty while providing their children with the necessary resources.

In addition to these specific programmes, several broader policies can help to prevent poverty, such as:

- Minimum wage laws: These laws set a minimum wage that employers must pay their workers, which can help ensure that workers earn enough money to support themselves and their families and prevent poverty.

- Education and training programmes: These programmes can help workers develop the skills they need to get well-paid jobs and earn a living wage, which can help prevent poverty by increasing their earnings potential.

- Job creation programmes: These programmes can help create new jobs and opportunities for low-skilled workers or people facing long-term unemployment. This can help prevent poverty by increasing the number of people earning labour income in vulnerable households.

The importance of government intervention in providing families with endowments that they can use to protect themselves from shocks becomes clearer when we focus on the geographical context of the household. In low- and middle-income countries, a substantial distinction can be made between households in rural areas and those in urban areas. Rural areas often do not have essential services that guarantee a certain quality of life, such as electricity or gas, drinking water, and internet. There are also fewer insurance and banking systems that cushion the impact of shocks and thus reduce risks. In addition, the main activity in rural areas is usually agriculture, livestock, or mining, which are purely extractive activities that are very susceptible to variations in the weather and prices. All these factors, determined by the geographical area, contribute to spatial inequality, and leave those families more exposed and vulnerable to poverty.

Exercise 6 Taxation, vulnerability, and inequality

Consider a tax applied to the entire population regardless of income level (for example, all households pay 20% of their income as tax).

What impact would this policy have on a) vulnerability, and b) inequality? Clearly state any assumptions you make.

The role of mitigation mechanisms in preventing vulnerability

In the context of our tipping point model, mitigation mechanisms play a pivotal role in stabilizing individuals within the vulnerability zone (Figure 4). In low- and middle-income countries, there is a significant concentration of vulnerable people on the left side of the vulnerability zone who are thus susceptible to falling into poverty due to any negative impact, no matter how small. These mechanisms, such as social assistance programmes, financial inclusion networks, and access to health and education services, are designed to position individuals at the top of the vulnerability zone. They equip individuals with the necessary resources to resist negative impacts and, ideally, to move towards the middle class.

Research on vulnerability to poverty has grown significantly in recent years, with a clear understanding of its contributing factors and mitigation mechanisms. This approach has significant implications for policymakers, as it provides a foundation for designing interventions that can effectively reduce exposure to poverty. For example, studies have shown that through strategic investments in education and employment programmes, governments can empower households to increase their incomes and assets, reducing their vulnerability to poverty. Moreover, empirical analysis has shown that expanding social protection programmes can provide safety nets for households facing shocks and stresses. In addition, economists have explored how governments can promote policies that enable households to develop robust coping mechanisms, such as protecting community-based networks that safeguard households from risks through solidarity, reciprocal exchanges, or altruism among family members, friends, and neighbours (as discussed earlier in this section).

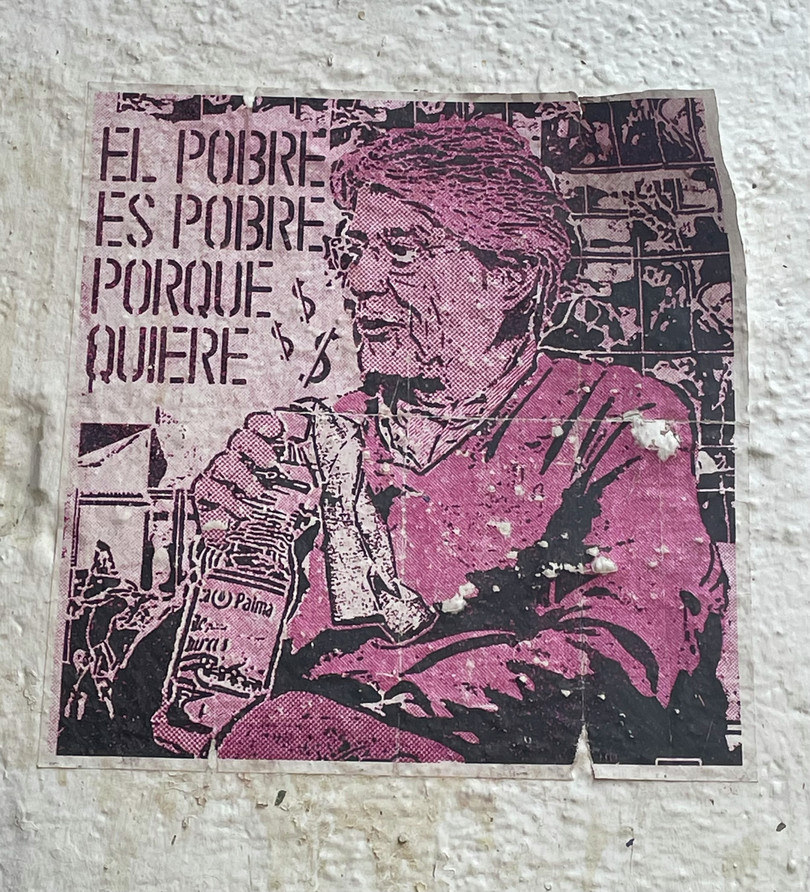

Find out more Do the poor choose to remain poor?

A piece of street art in Santa Marta, Colombia. It reads, ‘The poor are poor because they want to be.’

These ideas are based on the idea of meritocracy (the belief that a person’s position in society is primarily determined by effort and ability).

In a large research study with 6,000 households in Bangladesh, a team of economists tested the two major hypotheses of why the poor remain poor. One of these is based on the graffiti above, claiming that those below the poverty line are there because of their low skills or motivation. The other theory claims that those struggling to make ends meet are victims of poverty traps and face conditions that keep them in this bad equilibrium (as in the model from Section 2). Using a randomized experiment, these researchers found that the poverty trap hypothesis is a more plausible explanation. They showed how gaining a certain level of assets can trigger a cycle of asset accumulation, shifting households towards more productive occupations that push people out of poverty.3 Households that gain some assets below this level will not be pushed over the hill towards the middle class.

Conditional cash transfers (CCTs) have emerged as a global policy to assist the most economically disadvantaged individuals. These transfers are often contingent upon fulfilling specific requirements, typically related to education and healthcare. They are intended to act not only on monetary income, but also on household decisions helping to avoid poverty traps. Among the typical examples of CCTs are programmes in which children’s school attendance and education completion are compulsory in order to receive monetary transfers. By incentivizing low-income families to invest in their human capital, particularly by ensuring children’s attendance in school and access to adequate nutrition and healthcare, CCTs directly target the long-term alleviation of poverty. The focus on nutrition and education as conditions for receiving monetary assistance is widely supported, as it contributes to enhancing future earning potential and breaking the cycle of intergenerational poverty.

A large study conducted by the World Bank in 2009 evaluated the effects of such CCTs and suggested that such transfers work and have positive impacts.4 These programmes reduced poverty and increased household consumption of more nutritious food. These programmes also did not reduce the participation of these households in the labour market, except for a drop in child labour. Regarding education, these programmes increased participation in the schooling system and reduced the gaps in access to education by those in the lower income brackets, and in some countries (Bangladesh, Pakistan, and Türkiye), reduced gender gaps in educational attainment.

One example from high-income countries is an experiment in the United States called ‘Moving to Opportunity’, in which households from high-poverty neighbourhoods were given vouchers to move to places with less dire conditions. The programme’s effects showed that children under 13 from relocated households increased their future income and their chances of attending college.5 However, the economist Raj Chetty’s work has shown that intergenerational mobility in the United States has been declining systematically.6 One indicator is the steady decline in the percentage of people earning more than their parents. Over 90% of people born in the 1940s earned more than their parents, and this percentage has dropped to 50% in less than half a century.

Overall, the evidence indicates that households generally do not remain poor by choice, but rather due to external factors that trap them in poverty and require a large ‘push’ (such as government intervention) to overcome.

Exercise 7 Do the poor choose to remain poor?

Both high-income and low-income countries have a percentage of the population living under the poverty line. Public debate remains on whether it is the government’s responsibility to provide aid to these more vulnerable groups. One argument relates to fiscal capacity: rich countries may have more access to tax revenues to fund these safety net programmes.

Discuss some other factors that may affect a government’s decisions on which policies to implement, how generous these policies are, and the policies’ potential impacts.

-

Besley, Timothy, Stephen Coate, and Glenn Loury. 1993. ‘The Economics of Rotating Savings and Credit Associations’. The American Economic Review 83(4): pp. 792–810. ↩

-

Vriens, Eva, and Tine De Moor. 2020. ‘Mutuals on the Move: Exclusion Processes in the Welfare State and the Rediscovery of Mutualism’. Social Inclusion 8(1): pp. 225–237. ↩

-

Balboni, Clare, Oriana Bandiera, Robin Burgess, Maitreesh Ghatak, and Anton Heil. 2022. ‘Why Do People Stay Poor?’. The Quarterly Journal of Economics 137(2): pp. 785–844. ↩

-

Schady, Norbert, Ariel Fiszbein, Francisco H. G. Ferreira, Niall Keleher, Margaret Grosh, Pedro Olinto, and Emmanuel Skoufias. 2009. Conditional Cash Transfers: Reducing Present and Future Poverty. World Bank Policy Research Report. ↩

-

Chetty, Raj, Nathaniel Hendren, and Lawrence F. Katz. 2016. ‘The Effects of Exposure to Better Neighborhoods on Children: New Evidence From the Moving to Opportunity Experiment’. American Economic Review 106(4): pp. 855–902. ↩

-

Chetty, Raj, David Grusky, Maximilian Hell, Nathaniel Hendren, Robert Manduca, and Jimmy Narang. 2017. ‘The Fading American Dream: Trends in Absolute Income Mobility Since 1940’. Science 356(6336): pp. 398–406. ↩